From PM to Venture Builder: The Definitive Guide to the Career Move Nobody Talks About (But Should)

A deep dive into the evolution of product management into corporate entrepreneurship — with frameworks, case studies, and a playbook for building new ventures inside established companies.

For years, the product manager role has been the closest thing to a founder within a large organization. PMs live and breathe the customer's problem, own the roadmap with a fierce sense of mission, and rally teams to build something from nothing. They are, in many ways, the soul of the product.

But for most PMs, the accountability ends at the git push. You're measured on whether you shipped the feature, hit the launch date, and moved the engagement metric. Not on whether you built a business. That's someone else's job.

But a new evolution of this role is emerging, one that closes the final gap between product ownership and business ownership. It's a role where the objective isn't just to build a product inside a company, but to build a company inside a company. It's called a Venture Builder, and it represents a critical new capability for established companies looking for their next horizon of growth.

This isn't a theoretical post about "innovation theater" or corporate labs that produce beautiful slide decks and zero revenue. This is a practical, no-nonsense guide for leaders on how to establish and leverage a real, structured venture building function — taking an idea from a whiteboard sketch to a standalone business with a P&L, a customer base, and a path to becoming a spin-out entity. In the age of AI, where small teams can achieve unprecedented leverage, this function is more accessible and more critical than ever before.

Part 1: The Macro Shift — Why Now?

Corporate venture building isn't new. Bell Labs, Xerox PARC, and Lockheed Martin's Skunk Works are all legendary examples of internal innovation hubs that produced world-changing technologies. But for decades, this model was reserved for deep-pocketed industrial giants with long-term R&D horizons. For the average company, it was simply too expensive and too slow.

That has changed. Radically.

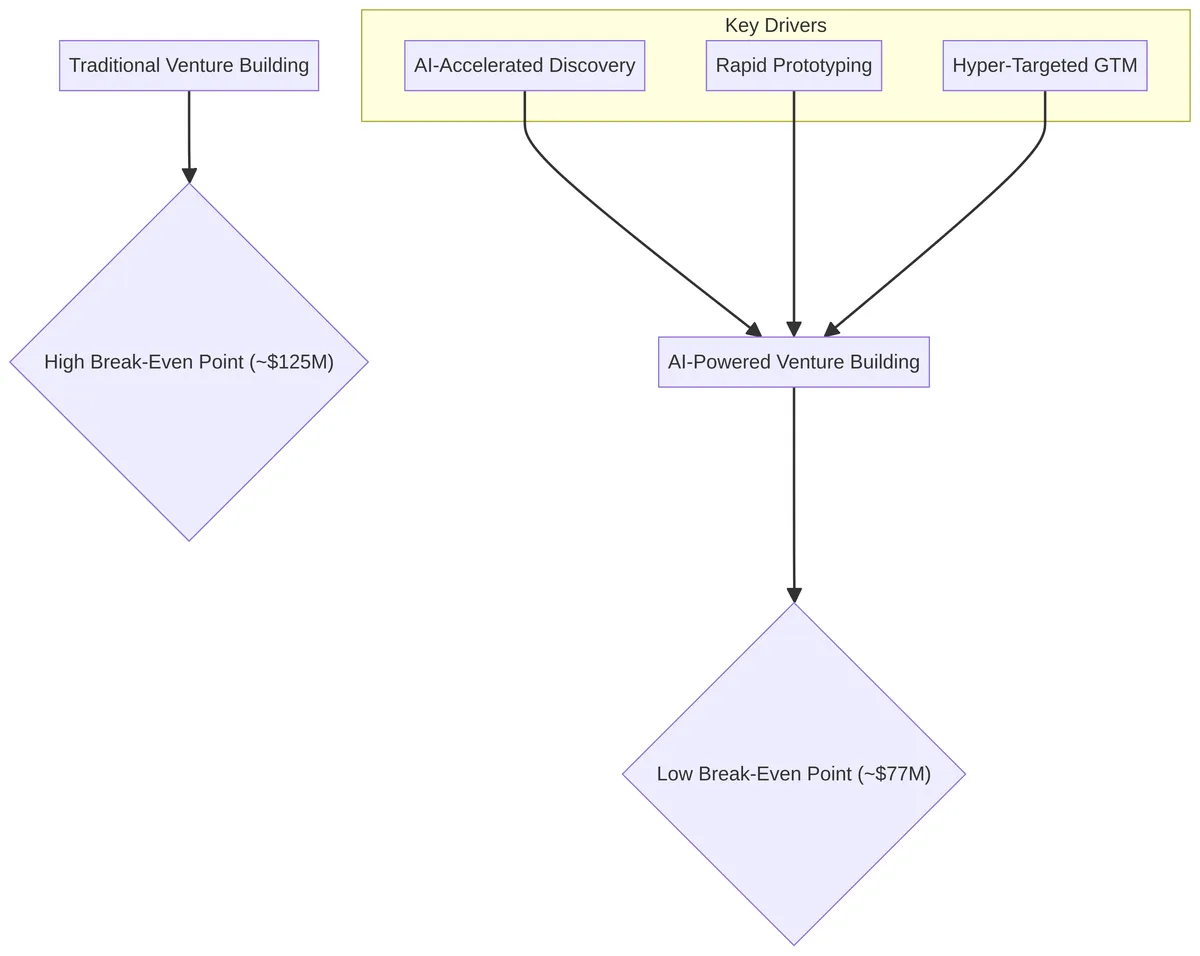

McKinsey's 2025 survey of over 700 senior executives paints a stark picture of this new reality. The average investment required before a new corporate venture breaks even has plummeted from approximately $125 million to $77 million in a single year. 1 This isn't a minor fluctuation. It's a seismic shift in the economics of innovation, driven almost entirely by the efficiency gains of AI.

The dramatic drop in break-even investment for corporate ventures, driven by AI-powered efficiency in discovery, prototyping, and go-to-market.

The dramatic drop in break-even investment for corporate ventures, driven by AI-powered efficiency in discovery, prototyping, and go-to-market.

The same survey found that 61% of new ventures now cross the $10 million annual revenue mark, up from 45% in 2023. And they're getting there 7 months faster, with the average time to that milestone dropping from 38 months to just 31. 1

What's happening under the hood? It's a confluence of factors, all supercharged by AI.

Compressed Discovery Cycles. What used to take months of market research, customer interviews, and competitive analysis can now be done in days. LLMs can synthesize market reports, analyze customer feedback for patterns, and identify white space with a speed and scale that was previously unimaginable. A Venture Builder can now run a first-pass market analysis in a morning and spend the afternoon talking to real customers.

Accelerated Prototyping. The gap between idea and interactive prototype has collapsed. With modern design tools, no-code platforms, and AI-assisted development, a Venture Builder can create a compelling, high-fidelity demo of a product in a weekend. This dramatically shortens the feedback loop and reduces the cost of experimentation. The old rule was "build it and they will come." The new rule is "demo it and see if they care."

Hyper-Targeted Go-to-Market. AI has made customer segmentation and acquisition surgically precise. A Venture Builder can now identify and reach a niche ICP with a level of accuracy that used to require a dedicated marketing team and a six-figure ad budget. Personalization at scale, once a luxury, is now table stakes.

The result is that the venture building model, once the exclusive domain of the Fortune 50, is now a viable growth strategy for any company willing to dedicate a small, focused team to it. And the person best positioned to lead that team is a product manager who is willing to trade the comfort of the product backlog for the ambiguity of the blank canvas.

Part 2: The Role — What a Venture Builder Actually Does

Let's be crystal clear about what this role is and isn't, because there is a lot of title inflation in the corporate world. "Venture Builder" can mean anything from a glorified project manager to a true internal founder. I'm talking about the latter.

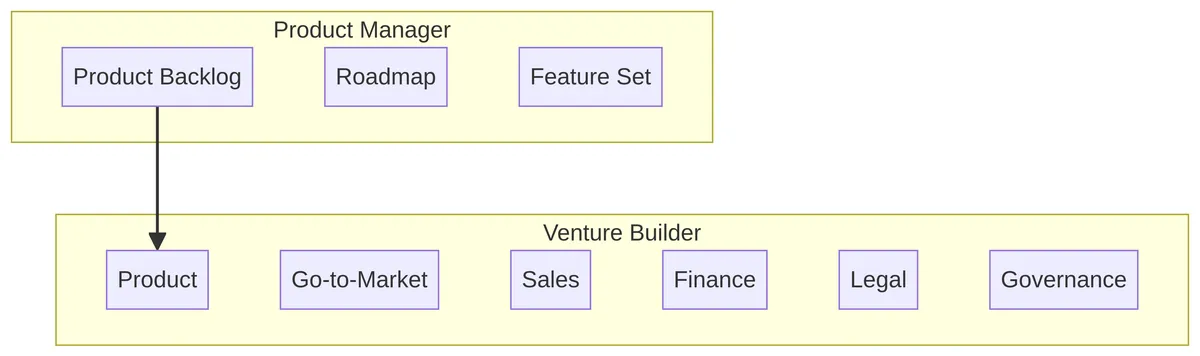

A Venture Builder is the single-threaded owner of a new business from inception to scale. You are the de facto CEO of a startup that happens to be wholly owned (for now) by a larger company. You own the P&L, you own the roadmap, you own the go-to-market, and you own the outcome.

The Venture Builder role encompasses the PM's product scope but expands it to include full ownership of GTM, sales, finance, and governance.

The Venture Builder role encompasses the PM's product scope but expands it to include full ownership of GTM, sales, finance, and governance.

The core mental model shifts from shipping features to building a business. That sounds simple, but it has profound implications for how you spend your time and what you value.

| Dimension | Product Manager | Venture Builder |

|---|---|---|

| Primary Goal | Ship a successful, high-quality product that users love. | Build a scalable, profitable business that can stand on its own. |

| Scope of Ownership | Product backlog, roadmap, feature set, user experience. | The entire venture: product, GTM, sales, finance, legal, governance. |

| Key Performance Indicators | Engagement (DAU/MAU), retention, conversion rates, NPS. | Revenue, CAC, LTV, gross margin, spin-out readiness. |

| Time Horizon | Quarters. Focused on the next release cycle and roadmap. | Years. Focused on the 1-3 year path to a sustainable business. |

| Core Decision-Making | Feature prioritization, roadmap trade-offs, sprint planning. | Kill/continue/pivot decisions, funding allocation, spin-out strategy. |

| Accountability | To the product organization and leadership. | To a P&L and an internal board. |

As a PM, your instinct is to build. As a Venture Builder, your instinct has to be to validate. You have to fall in love with the problem, not your solution. You have to be willing to kill your darlings. In fact, killing projects that aren't working is one of the most valuable things you can do, because it frees up capital and talent for the ones that are.

Part 3: The Skills Map — Bridging the Gap from PM to VB

A strong product management background is genuinely the best preparation for venture building. You already have the foundational skills. But there's a gap, and being honest about that gap is the first step to closing it.

Core PM skills are transferable, but the Venture Builder role requires building new capabilities in sales, GTM, finance, and governance.

Core PM skills are transferable, but the Venture Builder role requires building new capabilities in sales, GTM, finance, and governance.

What You Already Have (The Foundation)

Deep Customer Empathy. You know how to get out of the building, talk to users, and understand their world better than they understand it themselves. This is the bedrock of any successful venture. The discipline of structured customer discovery — separating signal from noise, identifying patterns across interviews, and resisting the urge to pitch before you've listened — is something most PMs have already internalized.

Hypothesis-Driven Frameworks. You're comfortable with ambiguity and know how to structure it. You can take a messy, undefined problem space and break it down into a series of testable hypotheses. This is the core operating system of a Venture Builder. Every week is a series of experiments, and your job is to design them well and read the results honestly.

Influence Without Authority. You've spent your career convincing people who don't report to you to do things they don't have to do. In a lean venture team, where you're constantly begging, borrowing, and stealing resources from the parent company, this skill is your superpower. The ability to build coalitions and move people without formal authority is the difference between a venture that gets things done and one that dies in committee.

MVP Mindset. You understand the art of the minimum viable product. You know how to ship something small but complete that delivers value and allows you to learn. This is crucial for managing burn and iterating quickly in the early stages of a venture.

The Gap You Need to Close (The New Muscles)

Founder-Led Sales. This is the big one, and it's worth dwelling on. As a PM, you've probably never carried a quota. You've never had to ask a customer for money. You've never faced the visceral, personal rejection of a lost deal. In the first 6-12 months of a new venture, you are the sales team. If you're not willing to do it, you're not ready to be a Venture Builder.

The good news is that PMs are actually well-positioned to become good at founder-led sales, because the best sales conversations look a lot like discovery interviews. You're not pitching; you're diagnosing. You're asking questions, listening carefully, and then showing the customer how your product solves the specific problem they just described to you. That's a skill PMs already have. The uncomfortable part is asking for the money at the end.

Go-to-Market from Zero. As a PM in an established company, you have the immense privilege of an existing distribution channel. You launch to an existing user base, with an existing brand, through an existing sales team. In a new venture, you have a blank slate. You need to figure out: Who is my ICP? Where do they live online and offline? What channels can I use to reach them? What's my pricing and packaging? How do I build a repeatable sales motion? This is a completely different discipline from launching a feature to an existing user base.

Financial Modeling and Unit Economics. You need to learn to speak the language of the CFO. Can you build a three-statement financial model? Do you understand the relationship between CAC, LTV, and payback period? Can you model the impact of churn on your revenue projections? For AI products, this gets even more complex: you need to model your inference costs and how they scale with user growth. You don't need to be a finance wizard, but you need to be fluent enough to have a credible conversation with an investor or a CFO.

Governance and Legal Structure. This is the stuff that seems boring until it blows up in your face. How should the venture be structured legally? Who owns the IP? How do you design a compensation and equity plan that motivates a founding team without creating legal or tax complications for the parent company? You'll work with legal and finance on this, but you need to be the one driving the conversation and understanding the trade-offs.

The Psychology of Killing. This is the hardest skill to learn because it goes against every instinct that makes a good PM. You're trained to be a champion for your product, to will it into existence against all odds. As a Venture Builder, you have to be a dispassionate capital allocator. The companies that are best at venture building are the ones that kill the most ideas fastest. It's brutal, but it's the job.

Part 4: The Playbook — A Step-by-Step Guide to Launching a Venture

Let's make this concrete. Here's a detailed, phase-by-phase walkthrough of how a Venture Builder would take an idea from concept to potential spin-out. We'll use a realistic case study: a Series B cybersecurity company that specializes in network segmentation has identified a potential new venture in AI-powered compliance automation for their existing enterprise customers.

The setup is classic: the opportunity is adjacent to the core product, it has a different ICP and pricing model, and it would distract from the core roadmap if built internally. The parent company has strong distribution (an enterprise sales team with deep relationships in financial services and healthcare), proprietary data (network telemetry and policy data from thousands of deployments), and deep workflow integration (the product is embedded in the customer's security operations). These are exactly the ingredients for a defensible AI-native venture.

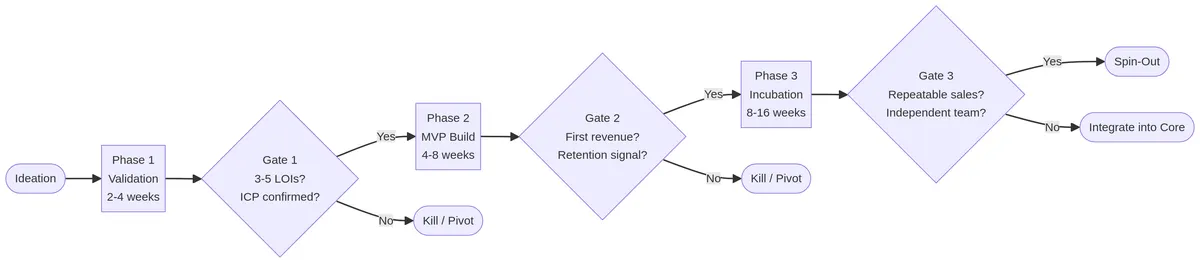

The three-phase venture lifecycle with explicit go/no-go gates at each stage. Most ideas should be killed at Gate 1.

The three-phase venture lifecycle with explicit go/no-go gates at each stage. Most ideas should be killed at Gate 1.

Phase 1: Validation (Weeks 1-4) — The Search for Pain

Objective: To validate that a specific, painful, and valuable problem exists for a well-defined customer segment, and that people will pay to have it solved.

Team: Venture Lead (you), 0.5x UX Researcher or Designer.

Week 1: Internal Discovery. You start by interviewing your own customer-facing teams — sales engineers, account managers, and support staff. You're looking for recurring themes. "I keep hearing from CISOs in the financial services space that they're struggling with GDPR compliance reporting. It's a manual, six-week process for them every quarter." You're looking for the whispers of a problem that's just outside the scope of your core product.

Weeks 2-3: External Discovery. Now you go talk to those CISOs. You schedule 20-30 interviews. You do not pitch a product. You do not talk about your company. You ask open-ended questions: "Walk me through your last GDPR audit. What was the most painful part? What tools did you use? If you could wave a magic wand and fix one thing about that process, what would it be?" You're listening for what I call "high-amplitude pain signals" — words like "nightmare," "I hate it," "it's a mess," or "I've been trying to solve this for years."

Week 4: Synthesis and Willingness-to-Pay Test. You synthesize your findings into a clear problem statement and a value proposition hypothesis. Then you test it. You create a one-page concept document that outlines the proposed solution: "An AI-powered platform that connects to your existing security stack and automatically generates GDPR compliance reports in minutes, not weeks." You go back to your 10 most interested interview subjects and ask for a commitment. Not a survey. You ask them to sign a non-binding Letter of Intent (LOI) to pilot the product for a specific price. "We're looking for 5 design partners to work with us on this. The pilot will cost $10,000 for three months. Are you in?"

Go/No-Go Gate 1: You need at least 3-5 signed LOIs or very strong verbal commitments from budget-holders. If you can't get this, you kill the project. No emotion, no ego. The market has spoken.

The most common mistake at this stage is confusing interest with intent. The LOI is the filter. It separates the polite from the committed.

Phase 2: MVP (Weeks 5-12) — The Search for Value

Objective: To build and launch a minimal, viable product that solves the core problem for your design partners and delivers measurable value.

Team: Venture Lead, 1x Tech Lead, 1x Full-Stack Engineer, 0.5x Designer.

Weeks 5-8: The "Concierge" MVP. You don't start by building a full-fledged product. You start by delivering the promised value manually. For our compliance reporting example, that might mean the Venture Lead and the Tech Lead spend a week manually pulling data from the customer's systems, running it through a series of scripts and GPT-4 prompts, and hand-crafting the final report. It's not scalable, but it allows you to test your assumptions about what a "good" report looks like before you write a single line of production code. This is the fastest way to learn what the product actually needs to do.

Weeks 9-12: The "Real" MVP. Based on the feedback from the concierge phase, you build V1 of the actual product. It does one thing and one thing only: it generates the compliance report. No fancy dashboard, no user management, no integrations. Just that one thing, done well enough that a customer would pay for it.

For AI-native products, this phase has some additional requirements that didn't exist a few years ago. You need to build your evaluation (evals) framework from day one. Create a "golden set" of test cases and measure the model's performance against them relentlessly. You also need to get a handle on your inference costs. How much does it cost to generate one report? Is that sustainable at scale? These aren't nice-to-haves. They're the difference between a product that scales and one that collapses under its own weight.

Go/No-Go Gate 2: You need at least 2 of your 5 pilot customers to convert to a paid contract and a clear line of sight to a gross margin of at least 60% at scale. If the product is a black box that costs more to run than you can charge for it, you have a science project, not a business.

Phase 3: Incubation and the Spin-Out Decision (Weeks 13-28) — The Search for Scale

Objective: To build a repeatable go-to-market motion and make a data-driven decision about whether to spin the venture out as a separate company.

Team: Venture Lead, Tech Lead, 2x Engineers, 1x Designer, 1x GTM/Sales.

Weeks 13-20: Building the Engine. You now have a product that works and customers who are paying for it. The focus shifts to building a repeatable engine for growth. The new GTM hire works with the Venture Lead to build a sales playbook, create case studies from your early customers, and generate a pipeline of new leads. The engineering team focuses on adding the features required to close the next 10 customers — basic user roles, an integration with a key data source, a proper onboarding flow.

Weeks 21-28: The Spin-Out Case. You're now running a small, self-contained business. You have revenue, a pipeline, and a roadmap. The Venture Lead's job is to package this up into a compelling business case for a spin-out. This includes a full financial model, a 3-year growth plan, and a proposal for the legal and equity structure of the new entity.

Go/No-Go Gate 3 (The Spin-Out Decision): You need a repeatable sales motion, a clear, independent roadmap, and a dedicated, self-sufficient team. If you have these three things, you spin out.

Part 5: The Metrics That Actually Matter

One of the most common mistakes in corporate venture building is using the wrong metrics. Teams track things that feel like progress — user signups, demo requests, feature usage — but don't actually tell you whether you have a business. Here's the framework I use across all three phases:

| Phase | Metric | What It Tells You | Minimum Threshold |

|---|---|---|---|

| Validation | Willingness-to-Pay signals (LOIs) | Is the problem real enough to pay for? | 3-5 LOIs or pre-orders |

| Validation | Interview-to-signal rate | How hard is it to find the ICP? | >40% of interviews confirm the problem |

| Validation | ICP definition clarity | Do you know exactly who you're building for? | Defined in one sentence |

| MVP | Activation rate | Are users getting value on Day 1? | >60% complete the core action |

| MVP | Week-4 retention | Are users coming back? | >30% still active after 4 weeks |

| MVP | CAC (initial) | How much does it cost to acquire a customer? | Benchmark against target LTV |

| MVP | Gross margin | Can you make money at scale? | >60% for SaaS |

| Incubation | Pipeline coverage | Do you know where the next 10 customers come from? | 3x pipeline coverage |

| Incubation | Sales cycle length | Is the sales motion repeatable and shortening? | Consistent, shortening over time |

| Spin-Out | Revenue run rate | Is there a real business here? | $500K-$1M ARR as a signal |

For AI-native products, two additional metrics are non-negotiable:

| AI-Specific Metric | What It Tells You | Minimum Threshold |

|---|---|---|

| Eval pass rate | Is the AI doing its job correctly at scale? | >95% on core tasks |

| Inference cost as % of ARPU | Can you make money at scale? | <10% of monthly revenue per user |

The inference cost metric is critical and chronically overlooked. I've seen teams build beautiful AI products that work perfectly in demos and then discover, at scale, that the cost of running the model is higher than the revenue per user. You need to model this from day one, not as an afterthought.

Part 6: The Governance Problem Nobody Solves

Here's the thing nobody tells you about corporate venture building: most ventures don't fail because the idea was bad. They fail because of internal politics, budget cycles, and the slow suffocation of bureaucracy.

I've seen it happen repeatedly. A team builds something genuinely promising, gets early traction, and then spends the next six months fighting for budget, navigating IP ownership disputes, and trying to figure out whether the sales team is allowed to sell their product. By the time they sort it out, the momentum is gone.

The solution is to establish clear rules of engagement before you start. Not as an afterthought, but as a prerequisite for the venture existing at all.

Budget and Runway. The venture needs a dedicated budget that's separate from the core product roadmap. A 3-month exploration budget with clear go/no-go gates is a good starting point. The key is that this budget is committed upfront, not subject to quarterly review. Nothing kills a venture faster than having to re-justify its existence every 90 days.

IP and Data. This is where things get legally complex. Who owns the IP developed by the venture team? What data from the parent company can the venture use, and under what conditions? These questions need to be answered by legal before anyone writes a line of code. The answers will shape everything from the venture's competitive moat to its ability to raise external funding.

Brand and Channels. Does the venture operate under the parent company's brand, an endorsed brand, or a completely new brand? This matters more than most people think. A venture that operates under the parent company's brand has instant credibility but limited independence. A venture with its own brand has more flexibility but has to build trust from scratch. The typical path is "endorsed brand first, own brand later."

Equity. This is the most sensitive topic, and the one that most companies get wrong. If you want to attract and retain a founder-level team, you need to offer founder-level upside. The most common model is an option pool in the spin-out entity, with a 4-year vesting schedule and a 1-year cliff. The options vest based on time, but there's often a KPI-based acceleration for hitting key milestones.

The worst thing you can do is ask people to take on founder-level risk without founder-level upside. I've seen this kill ventures that had everything else going for them. The team hits a rough patch, someone gets a competing offer with real equity, and suddenly you've lost your Tech Lead three months before launch.

Part 7: Why AI Changes the Math (But Not the Fundamentals)

AI has genuinely changed what's possible in venture building. A team of two or three can now build a working product in weeks that would have taken a team of ten a year to build. Customer discovery that used to take months can now be done in days. Competitive analysis that required a research team can now be done with a good prompt and an afternoon.

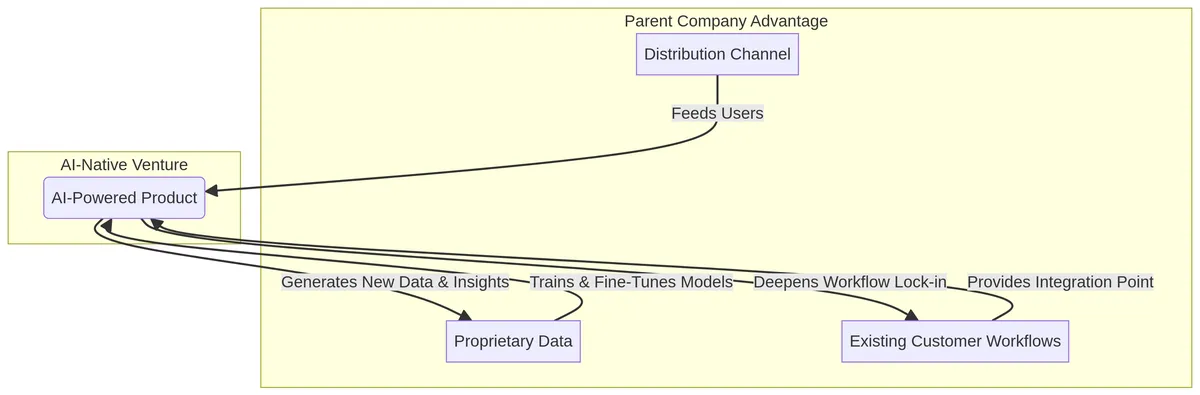

But AI hasn't changed the fundamentals of what makes a venture succeed or fail. The companies that are winning with AI-native ventures are the ones that have at least one of the following structural advantages:

A virtuous cycle where the parent company's distribution, data, and workflow provide an initial advantage, which the AI venture then deepens over time.

A virtuous cycle where the parent company's distribution, data, and workflow provide an initial advantage, which the AI venture then deepens over time.

Distribution. An established company has an existing channel to market. You have a customer base, a brand that people trust, and a sales team that can open doors. A standalone startup has to build all of this from scratch. This is a massive head start that most people underestimate. Getting your first 100 customers is the hardest part of building any business, and if you can skip that by leveraging an existing channel, you've removed the single biggest risk in the venture.

Proprietary Data. An established company is sitting on a mountain of data that a standalone startup could never replicate. This could be product usage data, customer support tickets, sales conversations, network telemetry, or operational metrics. This data, when used responsibly and with customer consent, is the fuel for building a differentiated AI product. A model fine-tuned on your company's unique data set will always outperform a generic model for your specific use case. This is a genuine moat. An LLM wrapper is not.

Workflow Integration. The stickiest products are the ones that are deeply embedded in a customer's daily workflow. An established company often has this already. A new venture can piggyback on this, building a product that feels like a natural extension of the tools the customer is already using. This creates high switching costs and a powerful network effect that a standalone startup would take years to build.

The failure mode I see most often is what I call "demo-driven development." The team builds a slick demo that wows executives, gets excited, and starts pitching it to customers. But when customers actually use it in production, the quality isn't there. The model hallucinates. The latency is too high. The cost per user is unsustainable. The product that worked perfectly in the demo falls apart under real-world conditions.

Part 8: Identifying and Cultivating Venture Builders

Identifying talent for a Venture Builder role is different from hiring a standard PM. The focus shifts from process and execution to judgment and resilience. When evaluating candidates, companies should be screening for three fundamental capabilities:

1. The Ability to Build from Nothing: The key question to probe is, "Tell me about a time you built something from 0 to 1." Look for stories that don't involve well-resourced projects with clear mandates. The best candidates will talk about navigating extreme ambiguity, making decisions with incomplete information, and hustling to get something off the ground. A great sign is a story that includes a near-death moment for the project and a clear articulation of why it was saved (or shouldn't have been).

2. The Capacity to Kill a Project: The counter-intuitive filter question is, "Tell me about a time you had to kill a project." A lack of a good answer here is a major red flag. The best candidates demonstrate an ability to separate their ego from the outcome and make a data-driven decision, even when it's painful. This shows they can act as a rational capital allocator, not just a passionate product champion. Bonus points are awarded for candidates who can articulate what they learned from the failure and how it informs their approach to new ventures.

3. A Bias for Selling: The final test is to ask, "How would you get the first 10 customers for this product?" This reveals whether the candidate thinks like a business owner or a product owner. A product owner will talk about features. A business owner will talk about distribution, pricing, and positioning. Look for specific, tactical answers: "I'd start by identifying 50 target accounts on LinkedIn, I'd use this email template to reach out, and my goal would be to book 10 discovery calls in the first two weeks." This demonstrates a crucial understanding that a product without distribution is just a hobby.

When using a case study format, the goal is to see if the candidate can structure their thinking around the venture lifecycle. Do they talk about validating the problem before jumping to solutions? Do they define the MVP in terms of learning, not just features? Do they define clear go/no-go criteria for each phase? The strongest candidates will naturally blend product thinking with business thinking, discussing the business model, GTM, and unit economics with the same fluency as the feature set.

Part 9: A Framework for Establishing a Venture Building Function

For leaders looking to build this capability, the question is where to start. The answer is not to create a large, top-down "innovation lab." The answer is to start with a single, well-defined business case and a single, empowered leader.

Step 1: Identify the Opportunity. The process begins by identifying a high-potential market adjacency that the company is uniquely positioned to win, but that doesn't fit neatly into the current product roadmap. The best opportunities are ones where the company has an unfair advantage — existing customer relationships, proprietary data, or a distribution channel that a standalone startup couldn't replicate.

Step 2: Develop a Lean Business Case. This opportunity should be captured in a concise, 5-slide business case. It should cover the market size and problem; the target customer; the proposed solution and business model; the company's unfair advantage; and a clear "ask" for resources.

Step 3: Fund a Time-Boxed Experiment. The initial investment should be small and de-risked. Instead of a multi-million dollar budget, fund a 4-6 week validation sprint with a lean team. Frame it as a low-cost experiment with a huge potential upside and clear, pre-defined go/no-go criteria. This approach fosters capital discipline and makes the initiative much easier to approve.

Step 4: Empower a Single-Threaded Leader. This is not a committee-led effort; it requires a single point of accountability.

The Bottom Line: Are You a Builder or a Business Builder?

The shift from traditional product management to venture building represents a significant evolution in how companies can innovate and grow. It requires a different mindset, a different skillset, and a different organizational structure to support it.

The individuals best suited for this role are those who are more excited by the question "should we build this?" than "how should we build this?" They are the product leaders who are already thinking like GMs, obsessing over business models, and building side projects just to see what's possible.

Conversely, this role is not a fit for those who are uncomfortable with extreme ambiguity, who shy away from the commercial realities of sales, or who require a clear roadmap to do their best work. Recognizing this distinction is key to placing the right talent in the right roles.

Venture building offers a powerful model: the upside of entrepreneurship with the safety net and unfair advantages of an established company. The trade-off is navigating the bureaucracy and risk aversion of the parent organization. Success requires a leader who can manage this tension effectively.

The path is not easy, but for companies that get it right, it's a powerful engine for growth. It's a way to take the immense talent that already exists within the product organization and apply it to the much harder, much more valuable problem of building new businesses.

Most companies will continue to focus on optimizing their core products. A few will build the capability to launch new ones. That is the opportunity that venture building presents.